Disclaimer: I have a small bag of $TLX, which will likely become vesting $SNX.

Success stories in DeFi can turn bittersweet overnight. The tale of $TLX – from its innovative launch to its unexpected finale – perfectly captures this reality. This is a story about investing in a project that builds something great, seeing it succeed, and watching it transform into something entirely different than planned.

What is $TLX

$TLX is the native token issued by the platform under the same name. $TLX holders have the right to elect protocol governors and earn 100% fees from the protocol based on the staked amount.

TLX protocol, the $TLX’s issuer, is a platform that allows users to trade leveraged tokens built on Synthetix.

Hold on – What are leveraged tokens? And what’s Synthetix? You might wonder. Below are the explanations for each one. If you’re in the know, skip to the next section.

What are Leveraged Tokens

The leveraged token is a financial derivative that allows traders to gain price exposure for an asset with a (relatively) fixed leverage without liquidation.

For instance, if you spend 1,000 USDC buying Bitcoin 3x bull tokens and the price of $BTC increases 5% soon after, the value of your position should now be 1150 USDC – a 15% increase – assuming no fees are charged. Conversely, if the price went the other way, the losses would be 3x’ed.

Most leveraged token platforms charge a streaming fee (based on how long you’ve held leveraged tokens) and a redemption fee incurred when you close the position. Few charge a mint fee when a trader opens a position.

There are two approaches to create leveraged tokens on-chain:

1. Using Money Markets

Indexcoop, afaik, is the first protocol that utilizes money markets like Aave/Compound to create leveraged tokens. Toros comes second.

Let’s use a Bitcoin 3x bull token to illustrate how to create a leveraged token. First, the protocol uses wBTC from its treasury and deposits it on a money market as collateral; afterward, the protocol borrows USDC against the collateral and gets more wBTC by swapping the borrowed USDC from DEXs. This process will be repeated till the target leverage has been reached. Now, the protocol can mint a wBTC 3x bull leveraged token representing such a position for traders to take.

You can also put 0xad38255febd566809ae387d5be66ecd287947cb9, which is the address of Bitcoin Bull 3x leveraged token from Toros, on Aave to see the latest composition – remember to switch the network to Arbitrum, though. Fun fact: most of the usage for Aave on Arbitrum is used by Toros to build their leveraged token.

The main benefits of using money markets to build leveraged tokens are

a. Users’ costs are lower as the borrowing cost on money markets is usually lower than the funding rates on derivative platforms.

b. Less bugs-prune as money markets and DEXs are simpler than derivative platforms.

2. Using Derivative Platforms

TLX is the first protocol to utilize liquidity from a derivative platform to build leveraged tokens, and Toros is second.

Unlike Indexcoop, which uses looping on money markets to gain leverage, TLX opens a leveraged position on Synthetix (a perpetual futures platform—more on it below) and mints a token representation (of such position) for people to take.

The benefits of this approach are:

a. If an asset is listed on the underlying derivative platform, you can create a leveraged token for it – even if that asset doesn’t exist on that blockchain.

b. More liquidity as derivative markets are more significant than spot markets.

————————————————————————————————————

No matter the approaches, the critical actions for leveraged token issuers are to 1) maintain each token’s leverage within a specific range and 2) prevent the positions from getting liquidated, as the selling points for such financial products are fixed leverage and no liquidation.

What’s Synthetix

Synthetix is an open-source derivatives liquidity protocol that has undergone multiple iterations. This article will focus on v2 on OP Mainnet.

On Synthetix v2, $SNX stakers collectively act as the counterparty for net positions from their traders. Suppose traders have a net long position, $SNX stakers are in a net short position, and vice versa. To compensate for the potential losses, stakers can earn from transaction fees collected from traders and (now concluded) token emissions. Additionally, they use position skew to calculate the funding rates – the higher the percentage of the long positions in the open interest, the higher the funding rates, and vice versa. By doing this, they incentivize people to open positions on the opposite side to reduce the net exposure for stakers and increase the transaction fees.

How did $TLX Launch?

The following are what the TLX team did before and after their token launch in chronological order.

A Targeted Airdrop

TLX launched a point airdrop for users who had been liquidated when trading Synthetix. This is brilliant as

- Synthetix users will likely be their users, and

- non-liquidatable leveraged trading is TLX’s unique selling point.

Additionally, the points are only claimable within 7 days after the announcement, which rewards active users on Twitter.

As a side note, to fund the initial developments, TLX raised some money from the following investors:

Multiple Token Utilities from the Get-go

The common problem with airdrops is that the tokens have no utility when one happens. As such, most people just dump the tokens whenever they receive them – as there is no reason to hold them.

Here is what TLX did after airdropping the tokens.

Lock to Earn $TLX Emission

Genesis Locking begins at token launch, and 4% of the total supply is reserved for Genesis Lockers. The rewards are distributed per block and claimable anytime during the first 26 weeks after the start of the campaign.

Bootstrap DEX Liquidity

Before starting this section, I must explain Velodrome. Again, feel free to skip it if you already know it.

What’s Velodrome

Velodrome is the largest DEX on OP Mainnet. It uses ve(3,3) tokenomics, allowing people to voluntarily lock up $VELOs in exchange for more voting power. The voters can then dictate which Velodrome pairs will receive $VELO token emissions (rewards for providing liquidity). Projects wanting to deepen their liquidity on Velodrome often bribe voters with their tokens, making people want to hold and lock up $VELO tokens.

The TLX team allocated some tokens as bribes for their $TLX/WETH pair on Velodrome. In addition to the bribes, I suspect they also bought some $veVELO from the community. The directed $VELO emission deepens $TLX’s liquidity, and provides an extra way to earn.

However, due to Velodrome’s voting schedule, $VELO incentives didn’t flow until one week after the token went live.

Stake to Earn $sUSD

The 100% revenue share for stakers kicked in instantly after the product went live – yes, they launched their tokens before their products.

Stakers can claim their shares of staking rewards in sUSD at any time. Likewise, stakers can unstake freely, but the amount will be subject to an “unstaking period” of 5 days.

Build Protocol-Own Liquidity (POL)

Another initiative TLX launched when the app went live was a feature called “bonding.” With it, people buy leverage tokens and give them to the TLX team; in return, they receive staked TLX at a discount.

This bonding mechanism has several benefits:

- TLX can use the leveraged tokens to build up their protocol-own liquidity (POL),

- It increases the transaction fees for stakers,

- It nudges users to keep the leveraged tokens within each leverage range, hence reducing operation overhead.

From time to time, devs behind TLX rebalance/liquidate the received leveraged tokens and split the proceeds for the following purposes:

- 20% is used to buy back $TLX, and the acquired tokens are put into a TLX/WETH pool on Velodrome,

- 80% goes to a wstETH/ETH1S pool on Velodrome.

The former is straightforward: It buys back $TLX from the market and builds up liquidity owned by the team, hence making liquidity “sticky.”

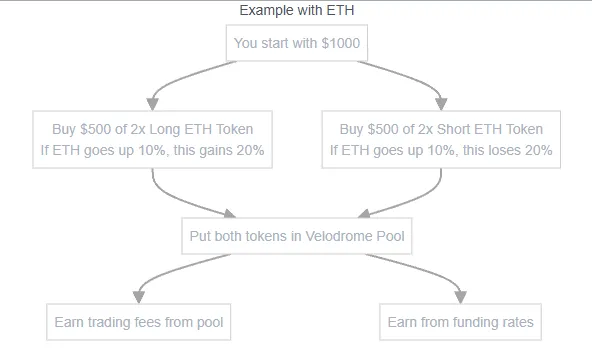

But what’s the wstETH/ETH1S pool?

ETH1S is the short token for ETH, meaning that if ETH goes 10% against USD, the price of ETH1S should drop 10% against USD. If you pair the same USD value of ETH1S and wstETH, you create a delta-neutral position where no matter whether ETH goes up or down against the USD, your deposit stays the same value in USD. This pool benefits three kinds of people at once:

- Stakers benefit from the streaming fees from the ETH1S tokens.

- Devs benefit from transaction fees from this pool and funding fees from ETH1S tokens.

I believe delta-neutral pools like ETH1S/wstETH are an underdeveloped area for this project. As the devs can potentially sell the LP tokens to people who want to earn fundings, like Toros’ delta-neutral tokens.

Quick Response to Market

One can plan many things, but ultimately, the market is the judge. Like Mike Tyson said, “Everyone has a plan until they get punched in the face.”

What makes the TLX team great is how fast they adapt to the market.

List/Delist Pairs Based on Volume

At launch, the TLX team listed leveraged tokens like SOL, BTC, and ETH, which had consistent trading volume on Synthetix. Later, they listened to the community’s feedback to determine which trending assets to list and with what leverage.

Besides listing new assets, the team periodically delists ones with limited usage to reduce operation costs.

Burn the Unnecessary Tokens

Unfortunately, the bonding scheme described above introduced too much selling pressure for $TLX. Backed by on-chain evidence, a community member proposed stopping the bonding scheme and burning the previously allocated tokens (a whopping 30% of the supply!) for the said feature. Given how well this proposal was received, the Tabby Council, the elected governors of the TLX protocol, eventually voted to pass this proposal. This reduction in supply makes $TLX more attractive to potential buyers as it reduces this project’s fully diluted valuation (FDV).

Why Bittersweet Ending

Reading this far, you might think, ” Things look great for this project. What do you mean, bittersweet ending?”

While everything seems to go smoothly, market dynamics have started to change.

In the past, Synthetix, the TLX’s liquidity source, decoupled its UI team and created another project called Kwenta that solely focused on building the UI for perpetual futures trading. This decision made sense back then due to faster execution and unknown regulatory risks, where Synthetix could concentrate on building the liquidity layer, and other teams like Kwenta could utilize the liquidity independently. To make this model sustainable, integrators received continuous integration fees paid out monthly from Synthetix. These integration fees came from the fees paid by the traders, hence making the service costlier than alternatives (only a handful of them back then).

Now that the competition for on-chain perpetual trading has intensified and a crypto-friendly regime will emerge in the U.S., Synthetix has decided to pivot from decentralization to vertical integration. We can see this transition from Synthetix’s Kwenta acquisition. After this acquisition, Synthetix essentially eliminated integration fees and consolidated the brand.

Seeing TLX’s success, Synthetix announced it would launch (delta-neutral) vaults and leveraged tokens next year. They proposed a “friendly” takeover for TLX to reduce the development time. As expected, it doesn’t look good.

This timing couldn’t be more perfect for Synthetix as:

- TLX protocol only supports one of the three chains that Synthetix is on. And the code audit for two other chains is still ongoing.

- The $TLX price has been distressed by whales’ (insiders?) selling pressure.

You can probably guess how “well” TLX’s community has received this proposal.

In response to the TLX community’s backlash, Synthetix has sweetened the acquisition proposal with the following amendments:

- SNX received in the conversion are subject to a 1 month lock and 4 month linear vest following the lock period.

- TLX tokenholders will receive a pro rata distribution of 700k stablecoins 6 months after the start date defined in the transaction contract. The distribution weighting will also account for the duration a converted TLX holder held their SNX claim in their conversion address.

At the time of this writing, the Tabby Council is still voting on this amended proposal, but it looks like it’ll be passed (see below). To be fair, I believe this is the right call, and I like Synthetix’s new direction. I’m just bummed by losing a token that 1) generates double digits real yields in stables and 2) can potentially go 100x thanks to low FDV. RIP $TLX 2024-2024.

I guess the moral of this story is that you should consider platform risks when investing in a token. If the underlying protocol is immutable, like Uniswap, you should be fine putting money into a token that builds on top of it. If that’s not the case, then you need to consider if any changes from the underlying protocol will rekt this investment.